This is the conclusion of my three-part series on how governments finance themselves. The aim is to clear up the popular misconception that the state’s budget is similar to that of a corporation or a household, that government borrowing is always necessarily a bad thing. Previously we talked about taxation and borrowing–today is all about printing.

To refresh, there are three dominant ways that states raise money:

- Taxation–they legally require their citizens to hand it to them under the threat of coercion.

- Borrowing–they request an amount of money and issue bonds to those who give it to them, promising to repay the money with some amount of interest. These bonds can be held by both citizens and foreigners.

- Printing–they print money and put it into the government’s account either directly or indirectly.

None of these methods of raising money is intrinsically immoral or irresponsible. It very much depends on the specific situation the government is in, and it is very dangerous to overgeneralize. There are a couple others ways to raise money that I decided not to cover, because they are not very common in the US or the UK today. These include collecting profits from state-run enterprises and seizing funds from other countries through conquest.

Printing

With both taxation and borrowing, the government has to take money from some people to finance spending elsewhere. When the government borrows money, it promises to return the funds it takes, but this takes time. Sometimes allocation of funds is not the issue–sometimes the sheer amount of funds in the economy is itself a major problem. How does this work?

Economist Paul Krugman explains this with a little parable about a babysitting co-op. In the babysitting co-op, a group of people agree to babysit one another’s kids, eliminating the need to pay cash to external babysitters. In theory, this allows all of the couples to leave the house more often while reducing their costs. But what if one couple in the babysitting co-op tries to take advantage of everyone else, constantly going out while trying to shirk their duty to babysit other people’s kids? There needed to be a system to ensure everyone does their fair share. Babysitting co-ops often solve this problem by issuing coupons entitling the bearer to one hour of babysitting time. To leave your kids with another couple for some number of hours, you have to give that couple an equivalent number of coupons.

The trouble is that the co-ops often do not issue a large enough number of coupons. Many couples try to save up their babysitting coupons so that they have enough for an emergency situation, and with a small number of coupons it is hard for every couple to be able to save up enough to feel comfortable. Because couples are anxious about running out of coupons, they go out less often, and this makes it harder for other couples to build up their reserves of coupons. So they too get more anxious and go out less often, and pretty soon no one is going out and no one is babysitting. The solution is to issue more coupons to the couples. By giving the couples more coupons, each couple feels less anxious about running out, so usage increases and the co-op is able to serve its intended purpose. It’s important to note that no one couple could rectify this problem by changing its individual behavior–the only way to solve the problem is for the central administration to issue more coupons.

The babysitting co-op story plays out on a larger scale whenever we have a recession. In 2008, defaults on housing loans caused many banks to suddenly realize that their assets were junk and that they had much less money than they previously thought they had. As a result, they tried to save money by reducing the amount of money they lent out, and this made it difficult for businesses and firms to get access to credit. Unable to raise more money through the credit markets, firms dealt with money shortages by trying to save money–mostly by reducing employment and cutting wages. This took money out of the hands of consumers, and consumers dealt with the money shortage by trying to save money themselves. This reduced sales for businesses and firms, causing them to try to save even more money by cutting wages and employment further, and so on in a vicious cycle. In this scenario, it makes sense for each individual actor to try to save money, but the aggregate consequences are disastrous for all the individuals participating. To satisfy the psychological urge to save without reducing consumption or investment, the state can respond by increasing the money supply.

This is not especially radical. Central banks do this all the time by lowering benchmark interest rates, encouraging banks to lend more money out. But if the economy is depressed deeply enough, the central banks may exhaust their ability to further lower rates. We can’t go below zero, so once the benchmark rate hits zero, the money supply must be changed by alternative means. In technical language, this is often called the “zero lower bound”, and once a country hits it, it is said to be in a “liquidity trap”. In the United States, the benchmark rate has been zero for years:

The same goes for the UK interest rate:

The Eurozone resisted dropping their rate for quite a while due to misplaced fears of inflation (contributing to the severity and awfulness of the Eurocrisis), but even its rate is now at zero:

Lowering the interest rate is also a very imprecise way for the government to intervene in the economy. Lowering rates generally encourages banks to lend, but it does not give the state any control over who receives that money. Lowering the rate doesn’t directly finance spending. Let’s say the government wants to do two things:

- It wants to increase the money supply rather than transfer funds from one part of the economy to another.

- It wants to control how the new funds are spent.

Taxation transfers funds. So does borrowing, despite the state’s promise that it will repay lenders at a later time. The only clear way out is for the state to print money and finance spending with that new money. Now, this is a genuinely radical move, and it scares people. People are very uncomfortable with the notion that the state can just print money at will. This is because historically this was not the case. Governments used to promise to redeem currency for a certain amount of gold–the famous “gold standard”. The gold standard prevented governments from engaging in radical printing or currency devaluations. This crippled their ability to respond to severe economic crises, but very rich people liked the gold standard because it made it harder for the government to engage in policies that would shrink the real value of their fortunes. The Great Depression made it clear that the gold standard could not be maintained in the face of a liquidity trap, and it was ditched. Now most countries have a system of fiat currency. This changes everything. States can print money now, and sometimes they do, but they are very careful to do it in a way that will not damage public confidence in the stability of the currency.

This is generally done through a process known as quantitative easing, or “QE”. QE can be used to finance government spending, but it can also be used to give more money to the financial sector. In QE, the central bank prints money and uses that money to begin buying bonds, either from the government directly at the time of auction or from the financial sector later on. This expands the money supply in one of two ways:

- It allows the government to quickly raise large amounts of money to finance new spending regardless of whether or not lenders are interested in financing that spending.

- It puts money into the hands of the financial sector, allowing it to potentially increase its lending activity.

The former sounds much more forceful than the latter, doesn’t it? There’s no guarantee that the financial sector will lend the money out, and it could always move the money to the wrong place (e.g. into another bubble or out of the country). This is why using QE to finance new spending is more controversial. Many countries have given QE a go. The United States has done a lot of QE, but this QE has not accompanied much in the way of fiscal stimulus, so its effect has been primarily to hand new money to the banks. The banks have done little with this money because there’s a lack of confidence in consumer spending because US consumers have seen stagnant wages for decades and have struggled to finance new spending without taking out potentially dangerous loans. Japan has done a lot of QE, and it’s been trying to use more of it to directly finance spending (though Japan’s shrinking population is a difficult obstacle for Japan to overcome, and the government has been tentative, undermining this policy with tax increases to allay debt fears). The UK has done QE as well–some estimates claim that UK GDP would have been 3% lower without it, and QE partially mitigated some of the negative growth effects of austerity. The Eurozone is just now planning to give it a try. But in many of these cases, the QE has been done primarily to put money back into the hands of the banks rather than to fund fiscal stimulus. This boosts lending, but excessive lending is what got the global economy into the crisis in the first place. QE has much greater potential than what we’ve seen. It has a bad reputation for increasing wealth inequality, but this is only because many states are are using it without the accompanying stimulus.

You’ll notice that regardless of how the government does QE, it still technically borrows money. The key thing is that it ends up owing this money to its own central bank. Whatever profits the central bank earns on the bonds it holds, it restores to the treasury. For example, the Federal Reserve handed the US government a record $98.7 billion in profits last year, essentially giving the government back its own interest payments. Similarly, in the UK, the Bank of England began doing the same thing, significantly reducing the government’s deficit. In many ways, this is an accounting dance meant to obscure what’s really going on. The government is printing money and using that money to expand the money supply, either by spending it itself or handing it to banks. The only serious constraint on its ability to do this right now is inflation. If the inflation rate rises substantially, the government will have provided all the demand and investment the economy can presently support. This hasn’t happened yet–inflation remains quite low. Indeed, the US is now experiencing minor deflation:

The same goes for the UK:

And the Eurozone has had the worst case of it:

All of this indicates that there’s likely significant additional slack. Governments could be increasing spending and money supplies further. Opponents might claim that because unemployment rates have fallen, this slack does not exist, but most unemployment measures exclude discouraged workers who are no longer looking for jobs and the underemployed, who are not making the best possible use of their skills. The US employment-population ratio still remains far below its pre-crisis level:

To be fair, as the boomers retire, we should expect to see some decline in the ratio, but not this much. As long as inflation remains low, it is reasonable to think that the ratio is depressed.

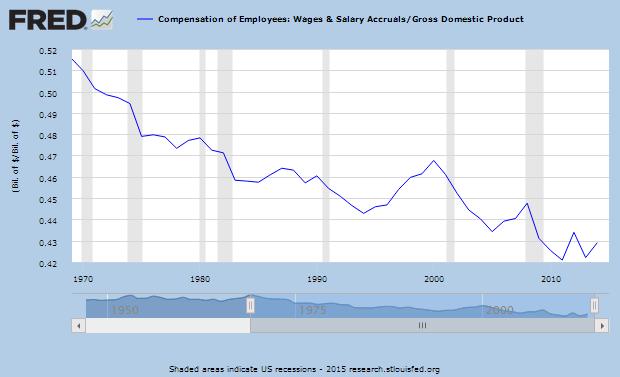

US wages have been in the toilet for decades, and this hasn’t changed:

Britain hasn’t had it as bad over the last few decades, but British wages are far from what they used to be too:

And British wages have performed especially badly in recent years–they have never performed so poorly over a seven year period in modern history:

So there’s quite a lot of room for printing to make a difference to the economy, provided that this printing is accompanied by fiscal policy that targets wage growth. While it’s true that the global economy forces rich countries to compete with low wage workers and that this can prevent wage growth, this only applies in the tradable sector, and most of the economy is still non-tradable (e.g. you can’t have a burger made for you in New York by people in Shanghai):

This means that most workers could see a significant rise in wages without seeing their jobs go overseas.

Our economy still isn’t performing at its potential. Wages are chronically lower than they ought to be, growth rates are weak and feeble, and inflation remains extremely low. Government spending can be used to intervene in all of these areas, and there are a variety of ways for the government to finance that spending with different advantages and disadvantages. Taxation encourages those taxed to save more and spend less and doesn’t expand the money supply, but the government never has to repay the funds and if it taxes the people with excess funds that are not being spent anyway, this is no great loss. Borrowing avoids discouraging the lender from spending, but it doesn’t expand the money supply. Printing allows everyone to have more money and feel prosperous, but it is constrained by inflation and it is sometimes co-opted by the financial sector, diverting money from consumers who could sometimes make better use of it. As long as these indicators remain what they are–as long as wages remain poor, the unemployment-population ratio remains depressed, and the inflation rate stays close to the basement–there is room for the government to take significant additional action to promote the general welfare.