Economists have gotten into a big fight with each other about the potential economic impacts of Bernie Sanders’ proposals. First Gerald Friedman came out with a new paper anticipating a tremendous improvement in economic performance under Sanders. Then four economists (Krueger, Goolsbee, Romer, and Tyson) affiliated with the Obama and Clinton administrations wrote a joint letter asserting that Friedman’s claims “cannot be supported by the economic evidence”. Paul Krugman subsequently took their side on his popular blog. Others have defended Friedman–Jamie Galbraith accuses the four of not having rigorously reviewed the paper, while Dean Baker claims that the New York Times is not giving Sanders’ side a platform and that there’s far more support among economists than we are being led to believe. In the popular press, this argument has rapidly devolved into a question of which authorities are more or less credible. I want to give you something better–a readable analysis of the actual arguments at stake here.

The big claim that everyone is focused on is Friedman’s growth rate projection for Sanders, which is significantly higher than the baseline rate (what is expected to happen without any big changes in current policy). Friedman thinks the annual GDP growth rate can increase from 2.1% to 5.3%:

Friedman gets these figures because Friedman thinks there is a large output gap, that the difference between current economic output and potential economic output is big. This is because he thinks the economy is demand-constrained. Ordinary working people have not seen significant real wage increases in a long time, and consequently their ability to consume additional goods and services without taking on debt has been limited. At the same time, productivity has been increasing:

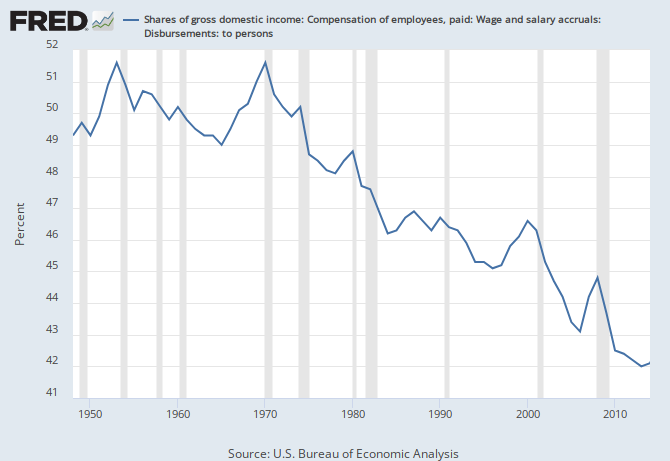

This means that the benefits of productivity increases have not translated into higher wages and have instead been shunted into investment. Indeed, since the 1970’s, the percentage of national income that has gone into wages has declined from around 50% to closer to 42%:

This wage decline’s impact on the growth rate was somewhat masked until the late 1990’s by rising workforce participation. The labor participation rate increased in the 80’s and 90’s because more women entered the workforce (even as the male participation rate declined throughout the period):

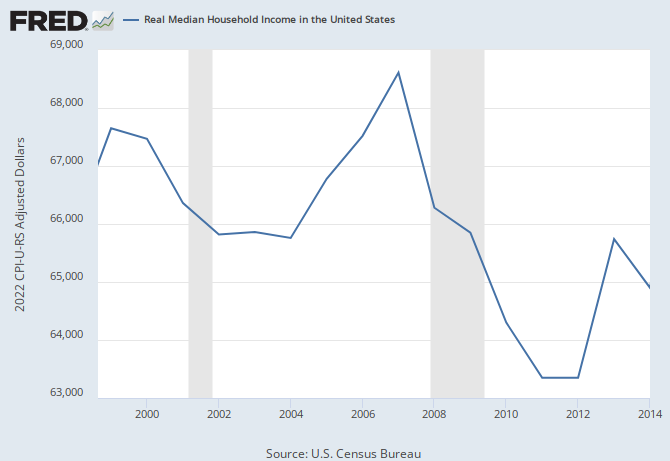

This means that the standard unemployment rate is somewhat misleading. The unemployment rate that is typically reported only includes people who are looking for work but cannot find any. It does not include discouraged workers, the underemployed, the early retired, or the incarcerated. Since 2000, real median household income has fallen along with the labor force participation rate (with the exception of the debt-fueled spike immediately before the 2008 economic crisis):

So Friedman thinks that Sanders’ policies can reverse the fall in household income by raising real wages and increasing workforce participation. This is meant to drive up the wage share of national income to get it back in line with historical levels. Specifically, he thinks we can get median household income up to 3.5% annual growth by increasing real wages by 2.5% annually and knocking the official unemployment rate down to 3.8%.

The extent to which you find this convincing depends on whether you think these figures I’ve been showing you are the result of deliberate policy choices or structural factors.

Deliberate policy choices might include things like allowing the real minimum wage to fall, weakening unions and driving down union membership, deregulating the financial sector and allowing its share of national income to increase to unsustainable levels, cuts to welfare spending and other forms of financial support that help consumer demand, reductions in effective tax rates on the rich that put more money in the hands of investors and less into the hands of consumers, free trade agreements that put US workers in wage competition with low-wage workers living in developing countries with minimal labor protections, etc. Friedman and his supporters think that these policy choices are doing most of the work, and by changing policy Sanders can change outcomes in large and powerful ways. Galbraith puts it this way:

What the Friedman paper shows, is that under conventional assumptions, the projected impact of Senator Sanders’ proposals stems from their scale and ambition. When you dare to do big things, big results should be expected. The Sanders program is big, and when you run it through a standard model, you get a big result.

Structural factors might include things like aging baby boomers, slowing or capital-biased technological change, and international competition due to globalization. Friedman’s opponents think that these structural factors make it impossible to produce the workforce participation rate from the 90’s or the strong wage growth we saw in the 50’s and 60’s, and consequently they don’t think we can achieve the high growth rates we used to see regularly in previous decades. Krugman thinks demography is the culprit:

much, probably most, of the decline in labor force participation since 1999 reflects an aging population

So let’s look at each of these structural factors in a bit more detail.

Demography: Aging Boomers

We know that there is still some slack in employment because when we look just at prime age workers (excluding people who are of retirement age), the workforce participation rate is still depressed by about three percentage points from where it routinely was in the 90’s (about 81% today vs about 84% then):

This compares to a gap of 4.5 points for the whole population (62.5% vs about 67%). This data suggests that at most retiring boomers account for just 1.5 of the 4.5 gap (that’s 1/3rd of it). That said, it’s possible that as time goes on and more boomers retire, demography could become a bigger drag on participation than it currently is. The median age of the US population is rising–from 32.8 in 1990 to 35.9 in 2001 to 37.8 in 2015.

But there are two deeper reasons to be highly skeptical of the demography argument:

- The first baby boomers were born in 1946 and turned 65 in 2011. This means the decline in workforce participation among men pre-2011 has nothing at at all to do with baby boomers retiring. In the 1960’s the male labor force participation rate was about 80%. It is now under 70%. Demography cannot be responsible for this 10-point gap. It’s either due to policy or some other structural factor.

- There is still a large gap between male and female workforce participation of more than 10 points. If this gap were to be eliminated or reduced, many more women could be added to the labor force.

If we could close the gender participation gap and bring male employment back in line with historical levels, we could potentially add 10 points to male participation and 20 points to female. That’s probably not realistic, because at least some of the reduction in male participation is the result of the increase in female participation, but Friedman doesn’t need us to lift participation that high anyway. His figures call for overall participation to reach 90’s levels (around 67%), not for participation to reach its hypothetical maximum if we returned male employment to near-historical levels and eliminated the gender gap (over 75%). I do not expect a 75% participation rate, nor do I think such a rate is possible under current conditions. But could Sanders reverse some of the long-term slide in male participation and/or close the gender participation gap to some degree, allowing his participation ceiling to be higher than Krugman anticipates? That’s very possible.

To be conservative, let’s assume that for other structural reasons, there is nothing Sanders can do about the long-term decline in the male participation rate. In the United States, female labor participation is 82% of the male figure. In the Scandinavian countries Sanders wants to emulate, it’s now 89% thanks to an array of government programs to help working parents. That alone would lift the female participation rate by about 6 points, which would increase the overall participation rate by about 3. Add this to the 3 points in prime age participation that we already know to be recoverable, and Sanders can pick up 6 points. This would give us over 68% participation, lifting us higher than the 67% 90’s figures that Friedman projects. If there is anything Sanders can do about the long-term decline in male participation, his participation ceiling rises higher still.

Technology

If you think that technological changes are capital-biased (i.e. they increase productivity by replacing labor), it’s by no means clear that this is immune to policy. If for instance we were to replace every worker in America with a robot, policymakers could respond to the collapse in employment and wages by taxing the owners of the robots and distributing the revenue to the former workers as a robot dividend or universal basic income. What’s more, if technological changes are capital-biased, higher taxes on the rich will have a minimal effect on job losses (because technology is already eliminating jobs), allowing Sanders to raise taxes and redistribute wealth easily with optimal consequences.

There are some however who take the pessimistic view that technology is not advancing as quickly as it used to and that this slowdown is a drag on growth. The most prominent tech pessimist is Robert Gordon. Gordon believes that technological and economic growth will slow as a result of six headwinds–demography, education, inequality, debt, environment, and globalization.

We’ve already discussed demography. Sanders has by far the strongest plan on climate change, and his tuition free college plan would eliminate student debt and increase educational attainment. Inequality is Sanders’ signature issue and by going after it he will reduce the need for households to take on unsustainable large debts to finance consumption in lieu of wage increases. If Gordon is right and technological progress is declining, no candidate is going to get very high growth rates, but we have reasons to think Sanders will do better than anybody else, and that’s what’s politically most important. Many critics are unsure if they share Gordon’s level of pessimism (here’s Krugman’s review of Gordon’s latest book).

There’s one last Gordon headwind to talk about…

Globalization

People tend to get carried away about globalization. The most important thing to remember is not how much things have changed, it’s how much still remains the same. 60% of the economy is in nontradable industries:

It’s hard to outsource services that have to be provided to people who are physically in the country. A New Yorker cannot buy a fresh Whopper made in Shanghai without going to Shanghai. So in 60% of our industries, we can increase wages without any risk of losing jobs to overseas competition. In the remaining sectors, policy choices are a big culprit–our governments have often cut trade deals with other countries that do not protect our workers from having their wages undermined by foreign workers protected by inferior labor laws. Trade deals could require our trade partners to implement stronger labor laws or permit tariffs or other restrictions to account for that difference. Indeed, this is the core reason Sanders is against TTP and has consistently opposed many other trade agreements that do not account for these differences.

What about the argument that Sanders’ tax policies could lead to capital flight or brain drain? Most of the programs Sanders wants to fund with these taxes are already operative in many European countries, yet these countries remain globally competitive. In its ranking of best places for business, Forbes ranks the US 22nd, behind a wide array of European countries, many of which pay for universal healthcare and tuition free college with higher tax rates. That said, all of these countries are losing revenue to rogue tax havens. Estimates for how much money is being lost to havens vary–some have put the figure at $150 billion while others have it at more than half a trillion in annual revenue for the US government alone. Eventually there will need to be international cooperation to stop countries from exploiting the rules. Thomas Piketty, who endorsed Sanders, has called for global agreements on tax rates. The rich countries will eventually need to get together and form a tax cartel, sanctioning states that fail to tax at minimum thresholds. In the meantime, the United States is a big and prominent market, and it can use that leverage to demand more revenue from corporations that use havens by denying those corporations access to the US market.

In the long-run, globalized trade requires globalized tax rates and globalized labor laws. To this point globalization has primarily been used to undercut the wages of working people in the rich countries and diminish their economic and political power. But if we radically change the governing ideology that has decided to implement globalization in this unnecessarily unhelpful way and begin globalizing tax and labor policy alongside trade, we can update our political toolkit, reign in transnational corporations, end the race to the bottom, and put governments back in charge.

So we have good reasons to think that policy might be doing a lot of the work here. Even many of the causes some economists label “structural” would still be responsive to sufficiently creative and innovative policy. And beyond that, there is clear evidence that we could have a smaller male/female participation gap and that much of the decrease in participation is unrelated to retiring boomers. Does this mean that Gerald Friedman is definitely right? No. We can and should have robust debates about the efficacy of policy and about the size of structural impediments. But asserting that the structural impediments are implacable and that anyone who disagrees must be making things up is an abuse of one’s platform and authority. It silences a debate we should instead be having.