I recently read a fantastic exchange between the German newspaper Die Zeit and French economist Thomas Piketty. Here is the original in German–there is an English translation by Gavin Schalliol, but at the time of writing Zeit is disputing Schalliol’s right to publish it. Fortunately, copies of the English translation have shared elsewhere on the web. In the exchange, Piketty makes a point that is seldom made–Germany itself is a direct beneficiary of the debt forgiveness and currency devaluation policies Keynesian economists are recommending for Greece.

Thomas Piketty is one of my favorite economists. He’s done excellent work on economic inequality and economic history.

In the interview with Zeit, Piketty had some poignant things to say about Greece and Germany:

Piketty: When I hear the Germans say that they maintain a very moral stance about debt and strongly believe that debts must be repaid, then I think: what a huge joke! Germany is the country that has never repaid its debts. It has no standing to lecture other nations.

ZEIT: Are you trying to depict states that don’t pay back their debts as winners?

Piketty: Germany is just such a state. But wait: history shows us two ways for an indebted state to leave delinquency. One was demonstrated by the British Empire in the 19th century after its expensive wars with Napoleon. It is the slow method that is now being recommended to Greece. The Empire repaid its debts through strict budgetary discipline. This worked, but it took an extremely long time. For over 100 years, the British gave up two to three percent of their economy to repay its debts, which was more than they spent on schools and education. That didn’t have to happen, and it shouldn’t happen today. The second method is much faster. Germany proved it in the 20th century. Essentially, it consists of three components: inflation, a special tax on private wealth, and debt relief.

ZEIT: So you’re telling us that the German Wirtschaftswunder [“economic miracle”] was based on the same kind of debt relief that we deny Greece today?

Piketty: Exactly. After the war ended in 1945, Germany’s debt amounted to over 200% of its GDP. Ten years later, little of that remained: public debt was less than 20% of GDP. Around the same time, France managed a similarly artful turnaround. We never would have managed this unbelievably fast reduction in debt through the fiscal discipline that we today recommend to Greece. Instead, both of our states employed the second method with the three components that I mentioned, including debt relief. Think about the London Debt Agreement of 1953, where 60% of German foreign debt was cancelled and its internal debts were restructured.

The London Debt Agreement of 1953 did indeed wipe out more than half of West Germany’s public sector debt. Germany also briefly unshackled inflation in the early 50’s, allowing its currency to fall:

The results were tremendous–Germany’s per capita GDP rose from about 45% of the United States’ in 1950 to 75% by 1960:

Some might argue that Germany was in ruins after World War II and that a recovery was inevitable in any case, but the speed of that recovery was dramatically affected by the elimination of Germany’s debt obligations. If we look closely at the above chart, we can see that the rate of improvement was significantly lower in the early 50’s than it was in the mid to late 50’s. Without this improvement, Germany’s economy would have crossed the 70% line around 10 years later than it did.

Growth also brought relief for Germany’s vulnerable. The unemployment rate dropped from double figures in the early 1950’s to less than 2% by the early 60’s:

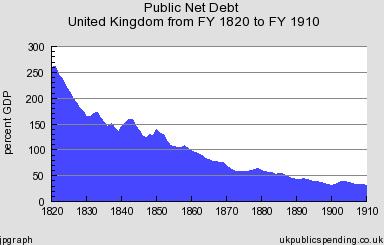

Piketty also points out that Britain followed an austerity policy after the Napoleonic Wars, with devastating consequences. Throughout the 1800’s, Britain declined to devalue its currency or resettle its debts, constantly trying to pay down its debt straight up:

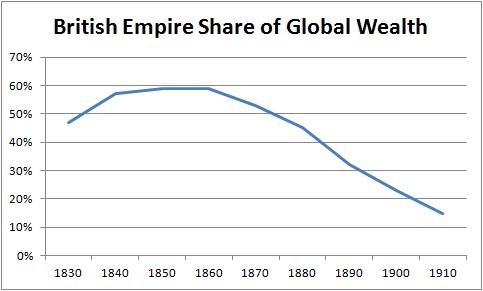

When a country is spending several percent of GDP on debt, it can’t invest that GDP in education, healthcare, infrastructure, technology, or other public goods. Britain was the first country to industrialize. It had huge economic advantages and it was excellent at manipulating trade agreements to keep ahead of rivals. But without public investment, no state can retain primacy indefinitely. The empire slowly bled, its standing among nations gradually diminishing:

Greece has very good reasons to prefer the debt forgiveness Germany enjoyed in the 1950’s to the long slog Britain endured throughout the 1800’s. Some have disputed Piketty’s analogy, alleging that Greece does not deserve the relief Germany received because of some long history of profligacy. But Piketty points out that this is unnecessarily cruel and punitive:

Piketty: To deny the historical parallels to the postwar period would be wrong. Let’s think about the financial crisis of 2008/2009. This wasn’t just any crisis. It was the biggest financial crisis since 1929. So the comparison is quite valid. This is equally true for the Greek economy: between 2009 and 2015, its GDP has fallen by 25%. This is comparable to the recessions in Germany and France between 1929 and 1935.

ZEIT: Many Germans believe that the Greeks still have not recognized their mistakes and want to continue their free-spending ways.

Piketty: If we had told you Germans in the 1950s that you have not properly recognized your failures, you would still be repaying your debts. Luckily, we were more intelligent than that.

Recent work indicates that it may not even be possible for Greece to reduce its debt burden with the British strategy. Paul Krugman has pointed out that under the austerity policies Greece has been implementing since 2009, its debt burden has gotten worse:

This is because spending cuts have damaged GDP far more than was initially predicted by the IMF:

Krugman raises the possibility that when we also take into account the way austerity lowers inflation, additional austerity for Greece might be unable to reduce Greece’s debt burden at all:

…a 1 point rise in the primary surplus, which requires austerity that causes a 3-point fall in real GDP, will reduce inflation by about 0.7 percentage points (3*0.23). And if you start with debt of 170 percent of GDP, this raises the debt ratio by more than a percentage point each year. That is, the attempt to reduce debt by slashing spending actually raises the ratio of debt to GDP, not just in the short run, but indefinitely.

If Krugman is right, the Victorian solution to Greece’s debt problems might not merely result in prolonged agony and slow impoverishment–it might not even accomplish its primary aim, the reduction of the Greek debt burden.

Piketty proposes a solution that could potentially keep Greece in the Euro:

ZEIT: What solution would you suggest for this crisis?

Piketty: We need a conference on all of Europe’s debts, just like after World War II. A restructuring of all debt, not just in Greece but in several European countries, is inevitable. Just now, we’ve lost six months in the completely in transparent negotiations with Athens. The Eurogroup’s notion that Greece will reach a budgetary surplus of 4% of GDP and will pay back its debts within 30 to 40 years is still on the table. Allegedly, they will reach one percent surplus in 2015, then two percent in 2016, and three and a half percent in 2017. Completely ridiculous! This will never happen. Yet we keep postponing the necessary debate until the cows come home.

ZEIT: And what would happen after the major debt cuts?

Piketty: A new European institution would be required to determine the maximum allowable budget deficit in order to prevent the regrowth of debt. For example, this could be a committee in the European Parliament consisting of legislators from national parliaments. Budgetary decisions should not be off-limits to legislatures. To undermine European democracy, which is what Germany is doing today by insisting that states remain in penury under mechanisms that Berlin itself is muscling through, is a grievous mistake.

This would make a big difference, but it’s doubtful that Germany is going to make this sort of proposal. Too many people mistakenly think that austerity is the only solution for Greece, when the reality is that it is at best a bad solution and it may not even be a solution at all. In the wake of the recent referendum rejecting austerity, it’s becoming increasingly likely that Greece will need to dump the euro and reintroduce the drachma. But it’s not over until the fat lady sings…