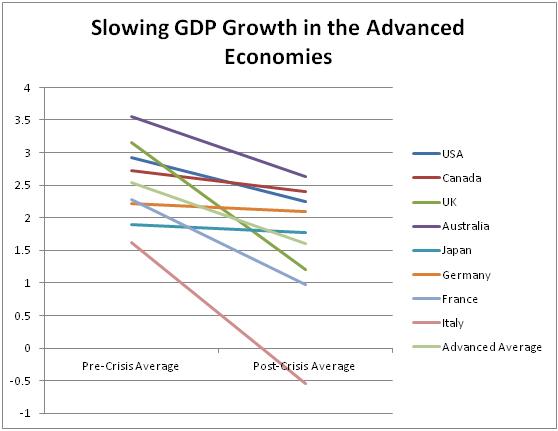

Since the global economic crisis of 2008, many of the world’s advanced economies continue to struggle to recover. In many of these countries, growth since the crisis has been much slower than it was in the years prior. Indeed, when we look closely, we see that the 2004-2007 growth average is higher than the 2010-2013 average in just about all the major advanced economies, and that in some countries this difference is very large:

What’s holding back recovery? To understand this, we need to understand what kind of economic crisis we’re trying to recover from in the first place.

When the economy is not doing well, it is usually either:

- Supply Constrained

- Demand Constrained

When the economy is supply constrained or “overheated”, this means that consumers have money and are ready and willing to buy goods and services, but suppliers are unable to provide enough goods and services to satisfy consumer demand. This can happen if employers are unable to hire the workers they need to expand production, and it can happen if there is a shortage of an important commodity, like oil. There are several reasons why employers might not be able to hire additional workers. There could be a skills shortage, unemployment might be too low, or wages may have risen too high. In all of these cases, the result is rising inflation—because suppliers cannot provide more goods and services at the same price level, they raise the price level until supply and demand are at equilibrium.

Depending on the cause of the supply shock, a supply constrained economy leaves different signatures:

- If the problem is a skills shortage, wages will rise rapidly in the particular skill area needed while inflation rises, in which case the state should incentivize people to acquire the requisite skills and potentially raise interest rates to stop inflation’s momentum.

- If the problem is low unemployment, wages will rise rapidly across the board while inflation rises, in which case the states should raise interest rates to increase unemployment and stop inflation’s momentum.

- If the problem is high wages, wages will rise or stagnate across the board while inflation rises, in which case the state should weaken unions and raise interest rates to stabilize wages and stop inflation’s momentum.

- If the problem is a commodity shock, the price of the commodity will rise rapidly while inflation rises, in which case the state should find a way to restore the supply of the commodity, seek a replacement for the commodity, and potentially raise interest rates to stop inflation’s momentum. A commodity shock can create inflation even when wages are stagnant and unemployment is high. This is called “stagflation”.

#2 and #3 often occur in tandem, though they don’t necessarily have to. In some cases, it can be hard to tell which one of these things is going on. During the 1970’s in the United States, there was much debate over whether rising inflation was being driven primarily by rising oil prices or by a combination of high wages and low unemployment. But in all of these cases, the key thing is that inflation rises. If inflation is not rising, the economy is not supply constrained. So how has inflation changed in the aftermath of the global economic crisis? Has it been rising? The short answer is no:

The only country examined to have a substantive rise in inflation is the UK, and even the UK inflation rate has fallen recently, from an annual high of 4.5% in 2011 to 2.6% in 2013. During the 1970’s, when the US economy was supply constrained, inflation rose into double figures. Even at the peak of the UK’s inflation in 2011, the rate did not top 5%. With inflation averages falling in the other countries (especially in the US), it does not look like the economic crisis was driven by a supply problem.

What about demand?

When the economy is demand constrained, this means that consumers do not have enough money to buy the goods and services required to support the economy’s growth. This happens whenever consumers’ incomes fail to keep up with economic growth. There are a variety of causes that often work together to undermine consumers’ incomes and create a demand crisis—high unemployment, underemployment, welfare cuts, state austerity, wage stagnation, and credit crunches can all play a role. An individual’s income available for consumption is typically fuelled by a combination of wages and borrowing, and a threat to either of these things undermines the individual’s income and consequently his capacity to consume.

We might remember that the global economic crisis was kicked off by a classic credit crunch. In the United States, homebuyers were frequently being issued “sub-prime” loans to people with limited incomes. Financial institutions believed that home prices would rise indefinitely, allowing borrowers who ran into trouble to sell their homes and recoup their debts. When the housing bubble burst, housing prices collapsed and many borrowers went “underwater”—the amount of debt they had on their homes exceeded the value of their homes. This meant that when people couldn’t repay their loans, they could not simply sell the house to someone for more money. Instead, they would have to default on their mortgages. Financial institutions failed to foresee this possibility, creating many “mortgage-backed securities” (financial products whose stability relied on mortgages) and circulating them throughout the global financial system. When the mortgages began to fall apart, the securities began to fall apart, and the banks that held those securities followed suit. With the banks in retreat, it became very difficult for consumers to take out affordable loans at reasonable interest rates. This limited consumers’ access to credit and depressed purchasing throughout the economy.

Governments all over the world responded with a series of bank bailouts. In effect, states assumed the banks’ debt obligations. This stopped financial collapse, but it put many states in difficult fiscal positions, resulting in austerity policies in many countries, particularly in Europe. These cuts to government spending have hurt income growth and hampered the economic recovery.

But why were Americans borrowing so much money in the first place? The left blames the banks for being too quick to offer people loans they could not afford, while the right blames the borrowers for accepting those loans. The reality is that the state failed to adequately regulate the system, allowing lenders and borrowers to make mistakes. Why did the state fail? Because, in recent decades, American economic growth has become increasingly dependent on borrowing. The debt load on the economy has ballooned since the mid-1980’s:

Why has the debt load grown so large? It turns out that when you adjust for inflation, US wages have not really grown at all for about 40 years:

As we said before, to grow the economy, consumers need to be able to buy additional goods. If consumers’ wages are not growing, the growth rate can only be sustained if consumers borrow more money to make up for the lost wage growth. The government was reluctant to regulate the financial sector to curtail borrowing because it needed the borrowing to maintain the growth rate. When things fell apart and borrowing collapsed, there was no substantive wage growth to cushion the blow, leading to a collapse in consumption. The advanced economies are still unable to recover from that collapse because wages have weakened further since the crisis:

So what’s the solution? To raise consumption, governments must raise consumers’ incomes. They can do this either by increasing borrowing or by increasing wages. As we’ve seen, trying to drive economic growth with borrowing is an inherently unstable enterprise. There simply isn’t enough wage income in the system to sustain the large debts that would be required to drive consumption with borrowing. Unfortunately, governments seem not to have learned this lesson. Governments have prioritized quantitative easing (QE), in which states’ central banks (e.g. the Federal Reserve, Bank of England, European Central Bank, etc.) buy bonds from financial institutions in exchange for cash. These policies put lots of money into the hands of banks with the hope that banks will once again begin lending it out at low interest rates. The trouble is that even if this works in the short run (and the evidence on this is mixed—banks seem to have become a bit more cautious, at least for the moment), in the long run consumers need a wage increase if they are to repay whatever future debts they incur. More borrowing is not the answer.

So how can governments raise wages? In effect, the government needs you to get a raise, and there are a variety of ways it can go about doing that:

- Raise the minimum wage, directly improving the consumptive abilities of poor workers while indirectly pushing up the rest of the wage scale.

- Expand union rights, increasing workers’ bargaining power.

- Increase government spending, creating high-paying public sector jobs.

- Cut taxes for the lower and middle classes, giving them more of their incomes to spend.

How does the government know when it has done enough? When the economy is no longer demand constrained, it will begin to show signs of being supply constrained, and that means inflation will rise. When inflation rises, that will likely mean that the government has done enough for consumers for the moment and needs to look for ways to help suppliers expand their capacity. It’s a balancing act.

NOTE:

I’m doing something a little different today–I’ve also posted a shorter, simpler version of this blog post as a YouTube video with the help of one of my friends, Micah Niedner. If it’s popular, I’ll continue to occasionally make blog posts that double as YouTube videos under the channel name “Polished Politics”. You can check it out here, and feel free to share it with your friends who don’t have the time or inclination to read extended long-form essays: