Italy finally has a coalition government–consisting largely of Lega Nord and the Five Star Movement, two Euroskeptic populist parties. The new coalition was elected to take Italy in a new direction, but this will prove difficult to do. Italy is a great example of what’s gone wrong in Europe. Let me tell you its story…

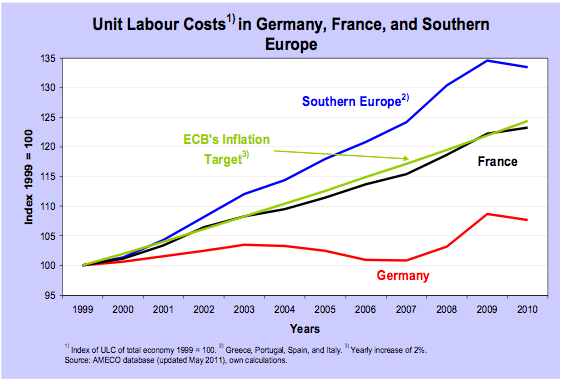

Italy, like most Southern European countries, spent the 00s buying German imports. The Euro, in combination with German labor market reforms, made it really easy for German products to outcompete native Italian goods. The German economy boomed in the 00s, and German firms put their profits into German banks, which then lent that money out to firms and governments in Southern Europe, allowing Southern Europeans to continue buying more German goods. This created a vicious cycle in which the Germans got rich and the Southerners went into debt:

You can see the German competitive advantage in its unit labor costs during the 00s:

When the housing crisis hit America in 2008, credit dried up all over the globe and economies contracted. This dramatically decreased the amount of money available to lend to Southern European countries like Italy. It also increased Italy’s debt as a percentage of GDP, both because Italy’s GDP shrank and because Italy was forced to prop up its economy with spending:

Italy’s unemployment rate doubled, and it hasn’t really come down since:

Perhaps most shockingly, Italy’s per capita GDP is now no higher than it was in the late 90s:

After two lost decades, the Italian people are miserable and sick of this stagnation. It is completely understandable that the mainstream parties no longer command the credibility or respect they once did. Italy has been trying to cut spending to get its debt to GDP ratio down:

But the spending cuts have damaged Italy’s growth rate. This starves Italy of tax revenue and makes it difficult for Italy to generate surpluses to shrink the debt in nominal terms. It also makes it harder for Italy to grow its GDP. Without GDP growth, it’s very hard for Italy to shrink its debt in real terms (i.e. relative to GDP). Italy needs to grow its economy to get the debt to GDP ratio down and to demonstrate to its frustrated people that it can take care of them. But how can Italy grow its economy? It needs a source of investment. The private sector has not been getting the job done over the last 10 years. But if the Italian state tries to fill in the gap, it will have to do more deficit spending. This would raise the debt to GDP ratio further in the short-term and it would break the European Union’s fiscal rules.

The EU does not wish to make more concessions on the fiscal rules for Italy. Italy has limited leverage in a negotiation with the EU because Italy relies on the European Central Bank (ECB) for quantitative easing (QE). The ECB uses quantitative easing to buy up Italian government bonds. This keeps Italy’s borrowing costs low. The interest rate the government must pay on 10 year bonds is significantly less expensive than it was before the QE policy:

If Italy breaks the fiscal rules, the ECB could stop buying Italian bonds, and interest rates could soar to destabilising high level we saw in 2011 and 2012.

France recently proposed an alternative. French President Macron, after demonstrating his good will by implementing labor market reforms long encouraged by the EU, asked German Chancellor Merkel to consider creating a European budget, which could spend money in Italy without the Italian government having to break the fiscal rules. This would effectively allow for the EU to raise funds from countries like Germany to spend them in countries like Italy, enabling Italy to effectively take on debt while federalising the cost of that debt across Europe. The Germans don’t like this idea–they call it a “debt union”, and Merkel rejected it.

This puts Italy in a very bad position. If it breaks the fiscal rules, it could lose the benefits of QE, and that could swiftly lead to a run on Italian bonds. If it can’t get the EU to federalise the spending, it has no other means of growing its economy or reducing its debt burden. The government would be forced to continue with most of the economic policies of the previous administration–it could only differentiate itself on social policy, by being more aggressively socially conservative. Unable to deliver real economic change, Italy’s new government may turn to race-baiting in a bid to make itself seem proactive. There is some evidence the new government already intends to pursue this route–the leader of Lega Nord, Matteo Salvini, has promised to build detention centers to round up and expel 500,000 people whom he alleges to be “illegal immigrants”. This policy won’t get Italians the economic growth they need, but it will make the government appear to be trying new things.

There are a couple alternative paths Italy might pursue. It could leave the Euro, in which case it would no longer be dependent on the ECB for QE–it could reintroduce the lira and devalue it, making Italian exports more competitive and shrinking the size of the debt in real terms. But this would very economically disruptive and it would make Italy’s bondholders very angry (as their bonds would quickly lose value). Recently Italy’s president rejected a proposed nominee for finance minister on the grounds that the appointee was “anti-Euro” and would anger investors:

Uncertainty over our position on the euro has raised alarm among investors and savers, Italian and foreign, who have invested in our government bonds and in our companies. The rising spread, day after day, increases our public debt and reduces government spending on new social initiatives. The losses on the stock exchange, day after day, burn the resources and savings of our companies and of those who have invested in them. And they configure a tangible risk for the savings of our citizens and for Italian families…It is my duty, in fulfilling the task of appointing the ministers, which I am entrusted by the constitution, to pay great care in protecting the savings of Italian citizens.

Effectively, the Italian president pronounced Italy’s subservience to the bond market and therefore precluded the possibility of exiting the Euro–at least until there is a new president, a new election, or a referendum on the issue.

The only other alternative for Italy is to attempt to engage in cross-national cooperation with other Southern European countries–in concert with France–to deliver some kind of ultimatum to the Northern Europeans and particularly to Germany. France so far has not been willing to confront Germany in this way. It has instead sought to make macroeconomic concessions to Germany in the hopes of future concessions on reforming the EU. This strategy always struck me as unlikely to succeed, and it now appears to be failing. If France wants the EU to change, it will need to stop making unilateral concessions and stand up to the Germans. It should talk to its counterparts in the South and see if they can take advantage of a moment in which there are now left wing governments in Portugal and Greece, a new center-left government in Spain, and a right wing but Euroskeptic government in Italy. Together, they might collectively bargain with the north for a better European deal.

Unfortunately, European political leaders have not been willing to push for this kind of fundamental structural change to this point. They are scared of the economic consequences of a showdown and prefer to see how many years of misery European peoples can endure before they lose patience with the system completely.

So Italy has four routes, and none of them are especially likely to go well:

- Break the fiscal rules and risk the wrath of the ECB

- Accede to the EU’s demands and create the illusion of meaningful policy change with loud racist social policies

- Leave the Euro, horrifying the bondholders and and precipitating an immediate economic crisis in the hopes of generating long-term growth

- Ask the French and the other Southern European countries to collectively bargain with it, even though they are probably too cowardly to say yes

The longer we leave Southern Europe to languish, the harder it will be to restore confidence in political and economic institutions in these countries. We risk the collapse of democracy in them and we risk the collapse of the European Union in them. At minimum, we risk many more years of misery, destitution, and stagnation for millions of people and the accompanying apathy and cynicism which might follow from that experience.

Northern Europeans don’t want to pay to help reduce the debt Southern Europeans acquired helping them get rich. But if the North doesn’t come around, the Southern markets may turn to nationalism and protectionism and deny the Northerners access to the markets which fuel their growth. Europeans need to recognise that the EU requires mutualism and interdependence–if Europeans don’t want the European economy to be a zero sum game, they can’t afford to play politics that way.