Today I’d like to take a mental trip back across the pond and examine the current double dip recession in the United Kingdom, investigating the role it plays as a case study in the policy debate between advocates of stimulus (state spending increases) and advocates of austerity (state spending decreases).

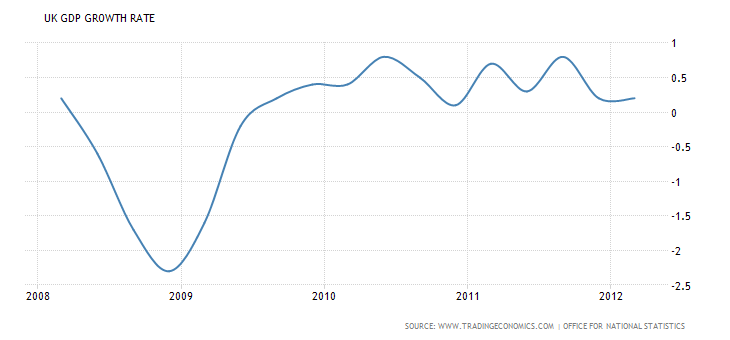

Like the United States, the United Kingdom suffered a severe recession driven by the global financial crisis. It’s then Prime Minister, Gordon Brown, and the ruling Labour Party embarked upon stimulus policies to try to turn the recession around. Under Brown, state spending as a percentage of GDP increased from 41% at the outset of the recession to 47% in 2010. However, Brown was defeated in the May 2010 election, and power passed to a coalition between the Conservative Party and the Liberal-Democratic Party led by current Prime Minister David Cameron. This coalition government promptly announced a policy of austerity due to fears that “bond vigilantes” would raise UK borrowing costs if this was not done, and out of a belief that the austerity would demonstrate the UK’s commitment to balanced budgets, creating an increase in investor confidence. Under this plan, state spending has to date fallen to 43.5% of GDP, and is expected to fall to 39% of GDP by 2016. Let’s see what impact all of this has had so far on growth in the UK:

As we can see, stimulus spending under Brown seemed to spurring a recovery, until around the time the new coalition government began implementing cuts. At first the growth fell off to stagnant, and now the United Kingdom is very clearly back in a small recession. The Labour Party, now in opposition, advocates “Plan B”, a return to growth promoting stimulus policies. The coalition continues to resist calls to change strategy both because the admission of austerity’s failure to restore growth would be an embarrassment to the government and because it still fears “bond vigilantes” punishing the UK for running high debt. The former concern is a political one and shouldn’t have any bearing on responsible government policy. The latter is provably overblown. Let’s look at some more charts:

Now, the coalition government likes to look at exclusively the bond figures since it took office, and claim that its policies effectively headed off an imminent explosion in UK borrowing costs, but if we look at figures that stretch back to 2008 prior to the Brown stimulus, we can see that bond costs were gradually falling even as Brown’s government was increasing spending.

Now, regular readers will recall that I often cite Paul Krugman’s observation that US 10 Year rates frequently are lower than inflation, and consequently negative when adjusted for inflation, meaning that the United States can borrow money at a profit. Seeing as the United Kingdom is also running an interest rate under 2%, is this also true there? Let’s have a look:

What we see here is that the inflation rate ran more or less together with the bond rate through the second half of 2010, and then the bond rate dropped under it. Effectively, the United Kingdom has found itself in more or less the same situation as the United States since some time in mid-2011, with the government capable of borrowing money for free for the purpose of stimulus since that point. This indicates that British concerns about “bond vigilantes” appear more or less unfounded–the market has tremendous confidence in UK ability to pay. This is no doubt helped by the British government’s control over its own currency through the Bank of England, which allows it to devalue it if necessary in order to reduce the size of its debt in real terms. The United States also possesses such a mechanism through the Federal Reserve, but Eurozone countries do not–they do not, individually, control the number of Euros in circulation or the interest rate on Euros, and so cannot manage their own monetary policies. This is the reason that Spain, a Eurozone nation with a similar debt burden to that of the UK, finds itself in so much more trouble than the United Kingdom does. Investors know that Spain cannot print more Euros of its own volition or alter its own interest rate, and worry that the European Central Bank will not guarantee Spanish debt. Hence, even though British and Spanish debt burdens are more or less the same:

This remains the case, even as interest rates on Spanish debt remain high, and interest rates on British debt remain low:

The mistake being made in the United Kingdom is the assumption that because debt levels in the United Kingdom and Spain are similar, the level of urgency that debt as a problem has is equivalent in the United Kingdom as it is in Spain. The British government either doesn’t understand or has chosen to ignore the fact that it has its own currency and its own monetary policy, which free it from the constraints that are presently ensnaring Spain. The United States’ debt to GDP ratio, set to hit 70% by the end of 2012, sits far below UK debt levels, making this example even more forceful in the American case–if the British, presently running a debt to GDP ratio of 90% (as indicated in the chart), can maintain bond interest rates under 2% and borrow money at profit, the United States has tremendous spending flexibility and could indeed be doing substantial stimulus at no significant cost. We find, once more, that the dangers of debt exist in the minds of policy makers, but not in the realm of reality.

Source List:

Guardian on UK Spending:

http://www.guardian.co.uk/news/datablog/2010/apr/25/uk-public-spending-1963

UK GDP:

http://www.tradingeconomics.com/united-kingdom/gdp-growth

UK Bond Rates:

http://www.tradingeconomics.com/united-kingdom/government-bond-yield

UK Inflation Rates:

http://www.tradingeconomics.com/united-kingdom/inflation-cpi

Paul Krugman on Spain/UK Comparisons:

http://krugman.blogs.nytimes.com/2012/08/24/gop-intellectual-decline-monetary-edition/