The fall of Silicon Valley Bank (SVB) generated several different media narratives. All seem to agree that SVB failed because it was dependent on low-yield long-term US treasury bonds. These bonds were safe in the years following the global financial crisis of 2008, but they lost value when interest rates increased in 2022. The disagreements are over what this fact means.

There are three different ways of assigning blame:

- SVB is to blame, because SVB could have diversified its holdings to reduce its dependence on these bonds, and it did not.

- Private banks are to blame in a general sense, because they pressure the Federal Reserve to keep interest rates low by maintaining portfolios that are only workable in a low interest environment.

- The Federal Reserve is to blame, because it raised rates when it knew that many banks – including SVB – are not in a good position to deal with rate hikes.

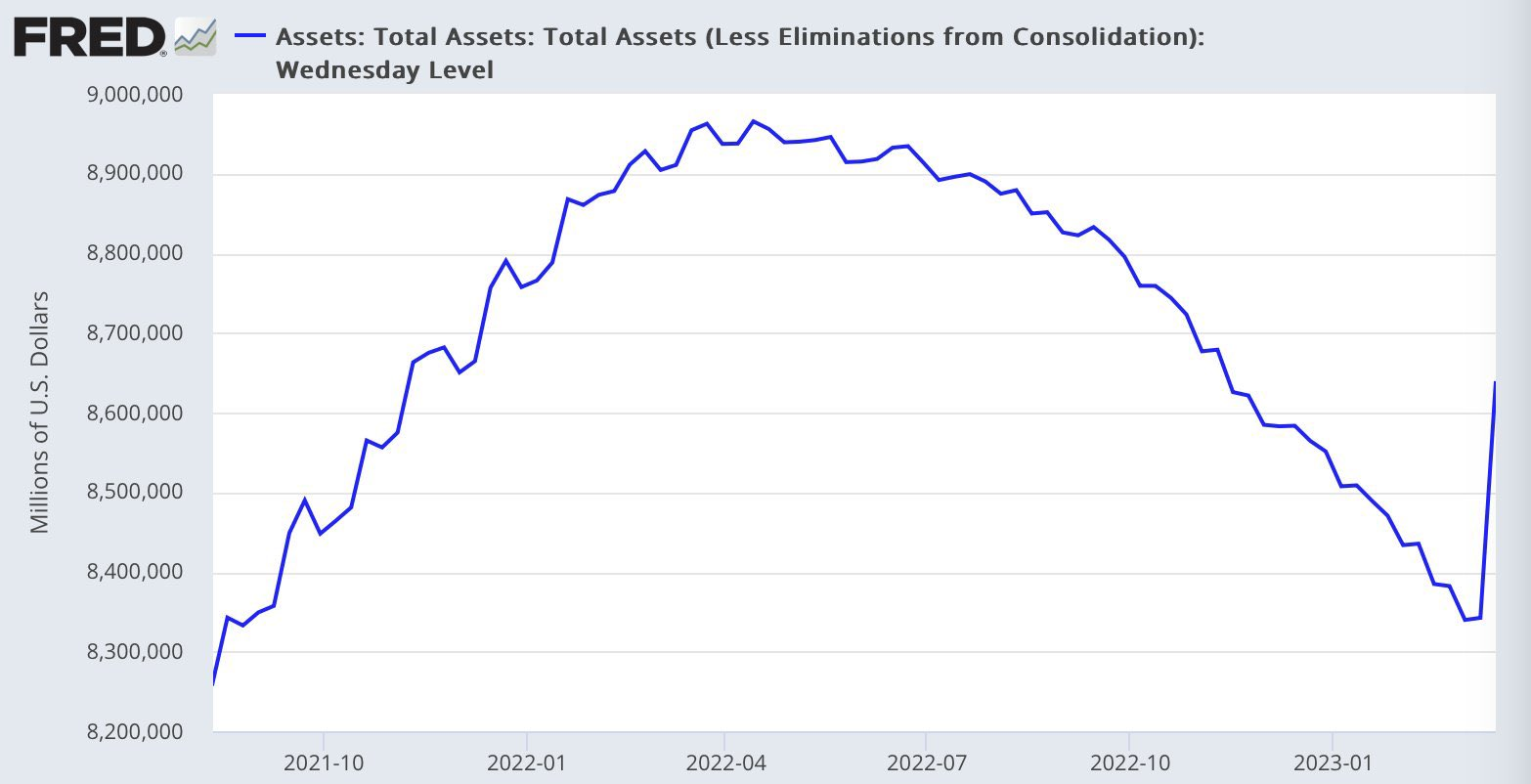

Each of these lines suggests a different policy response. If SVB alone is to blame, then there’s nothing fundamentally wrong with the Federal Reserve’s strategy and there’s no reason for it to abandon rate hikes. This can, however, be straightforwardly disproven, if the Federal Reserve presses ahead and more banks fail. If private banks are primarily to blame, rate hikes will only work if the banking system is redesigned. But since we have a divided congress and a president who is unable or unwilling to persuade his own party to vote for major reforms of this kind, it is not politically possible to take that kind of action. If the Federal Reserve is primarily to blame, then rate hikes have to be abandoned and/or the Fed must take other kinds of action to offset the effect of the rate hikes. As it happens, this is what the Fed has decided to do, quickly acquiring assets in a bid to recapitalize the banks:

Online, the discussion focused on who we prefer to blame and on the policies that are implied by the way blame is distributed. But in real politics, two material facts were more important:

- This isn’t just a problem for SVB. The financial system has become dependent on low interest rates, and it struggles to cope with rate increases.

- The US government lacks the state capacity to redesign the banking system.

In this environment, the only available policy option was for the Fed to ride to the rescue. This was the only response the American political system was capable of generating. At this point, the Fed is not merely the most dynamic part of the American economic policymaking, it is the only part that exhibits any dynamism at all. Whether the Fed is to blame is beside the point. The Fed is the only part of the system that can quickly change its behavior. Because the Fed is the only part of the state that can act, it is always as if the Fed is to blame. Insofar as ought implies can, only the Fed can do anything, so only the Fed ought to do anything.

The thing is, this is how we arrived at the low interest rate environment in the first instance. After the 2008 crash, there was a brief Keynesian “renaissance” in which states committed to fiscal stimulus. But very quickly states exhausted the political capacity to do stimulus. The right recognized in the 2008 crisis an opportunity to impose austerity policies by highlighting the size of the debts and deficits states accumulated. In Europe, rich states like Germany became unwilling to finance further stimulus in poorer states like Greece. In the United States, the Obama administration shifted gears and embraced the Budget Control Act of 2011, committing the government to years of austerity and budget cuts.

As states lost the capacity to do stimulus, the recovery flagged, and states became increasingly dependent on the ability and willingness of their central banks to step in. This intervention came in the form of permanent low interest rates and periodic cash injections via quantitative easing. The banks understood that as long as the state could not take other forms of action, low interest rates would have to prevail. The state could not make the large, long-term investments that would make low interest rates unnecessary, and it could not redesign the financial system to stop the banks from taking advantage of the low interest rate environment. In this situation the winners were those who most effectively exploited the low interest rate environment, engaging in forms of economic activity that, in any other situation, would have been clearly and obviously unproductive (e.g., crypto and NFTs).

All of this looked very sustainable from their point of view, because no matter what the Fed did in the 2010s, it could not for the life of it push the inflation rate past 2%. That all changed when the coronavirus attacked. By disrupting supply chains, the virus created shortages of various goods and services. Those shortages were exacerbated by a lack of coordination among governments. The United States reopened much faster than China, and that meant that American demand recovered much faster than Chinese production. There were shortages of, among other things, computer chips, cars, and essential building materials. Then Russia invaded Ukraine, kicking up oil and gas prices, and that put even more inflationary pressure on the system.

Stagnant wages in the last quarter of the 20th century left the United States in a poor position to finance further growth in living standards. The 2008 crisis made it clear that household debt could not substitute for wage growth indefinitely. But the American state lacked the capacity to organize the economy in such a way that wages could rise. So, it fell to the Fed to generate growth by creating an exotic financial environment in which the usual rules did not apply for an indefinite period. But exogenous shocks – from the pandemic and the war – kicked up inflation and made that exotic financial environment appear unsustainable. The Fed tried to get rid of it, only to discover that the economy has very limited ability to tolerate the kind of interest rates that were routine in the decades before the exotic period.

Now the Fed will fly through the eye of a needle, keeping rates as high as it can to fight inflation while using cash injections to protect the banks from the consequences of its strategy. In the meantime, the wage gains Americans won during the pandemic will be totally reversed. Over the last year, inflation has eaten away at them. Now, high interest rates will goose unemployment and diminish their leverage. This will make the situation worse in the long-term, as poor wage growth is the reason the economy became dependent on household debt and exotic financial environments in the first instance. But every time the Fed gets the economy through one of these periods, it becomes less clear that any real change is necessary. And so the structural situation slowly deteriorates, and global economic policy becomes more and more dependent on the technocrats that run the central banks. The people who govern central banks invariably come from the financial sector, and they manage these crises in ways that are friendly to former and future employers.

Every time this happens, dissenters will cry out that this is the fault of the banks, that the financial system needs to be redesigned. But there’s no state capacity to do that. At this point, it seems pretty clear that media professionals crying about the banks online is not enough to generate this capacity. But no one seems to have any concrete ideas about what to do, so we’ll have a cry and then move on to other, less relevant news stories.