The University and College Union (UCU)–Britain’s trade union for academics–has gone on strike. The strike is about the University Superannuation Scheme (USS)’s decision to switch academics from “defined benefit” pension plans to “defined contribution” plans. As a PhD student at Cambridge I write this piece at home, having skipped a couple events I really wanted to go to today, because this strike is so important, both to academia and to the cause of working people more generally. My hope is that I can explain the strike to those who don’t know much about it and defend it to any who doubt its necessity.

There are three broad reasons this strike is important:

- The contribution it makes to defending the right of all working people to retire comfortably.

- The contribution it makes to defending the quality and standing of British universities.

- The contribution it makes to defending and extending the capacity of working people in western democracies to protect their interests effectively through collective bargaining.

My intention is to do a piece on each one. This is Part I, which focuses on retirement and pensions.

The Right to Retire Comfortably

Under defined benefit plans, workers are promised fixed amounts of money when they retire no matter what happens. Under defined contribution plans, workers pay money into plans which invest in the stock market and are therefore subject to its fluctuations. USS wants to make this switch because defined contribution plans typically require much less money from employers, but they consequently pay out much less money to workers.

To get precise about this, UK employers pay an average of 15% of workers’ earnings into the pension scheme, while under defined contribution plans they pay less than 3%. This cuts employers’ contributions by 80% on average:

Early career academics (like yours truly) are projected to lose £200k on average over the course of their (our) working lives. In the post-war period most people in rich western countries had good, solid defined benefit plans. But in the 80s they started to pry them away from us, bit by bit, and now even public sector employees in cushy European countries have to go on rolling strikes to stand a chance at preserving them. Today only a small fraction of defined benefit plans remain, and some workers are having to do without pensions of any kind:

Now, the right often argues that the move away from defined benefit plans was inevitable, that they weren’t affordable to begin with. But most defined benefit pensions were doing fine pre-2008. Economic growth in the last 10 years has been below the mid-00s projections, and this has caused some of those pensions to come up short. The 08 crash was not the fault of the workers–it was caused by the investor class and by the states which encouraged the investor class to behave badly. But while the investor class gets bailed out by the state, when pension funds have shortages the state refuses to step in and tries to make workers eat the cost.

In this particular case the pension shortage may not even be genuine–there was no shortfall in the pension scheme until very recently, when USS changed the way it calculates its pension balance sheet. There are allegations that they may have done this under pressure from certain British universities with strong financial positions. These universities allegedly wanted to leave the pension scheme to reduce their liability in the event that weaker UK universities ran into fiscal trouble. Unable to do this, it is claimed that they instead pushed to have the fund recalculated to justify overhauling the system completely. This could widen the gap between the strongest UK universities and the system’s middle and lower tiers. I am not in position to verify any of this, but you can read a Medium piece by an LSE academic if you’re interested in the details. As far as I’m concerned, regardless of whether the deficit is real or contrived, it is wrong to make workers pay for mistakes made by investors and states.

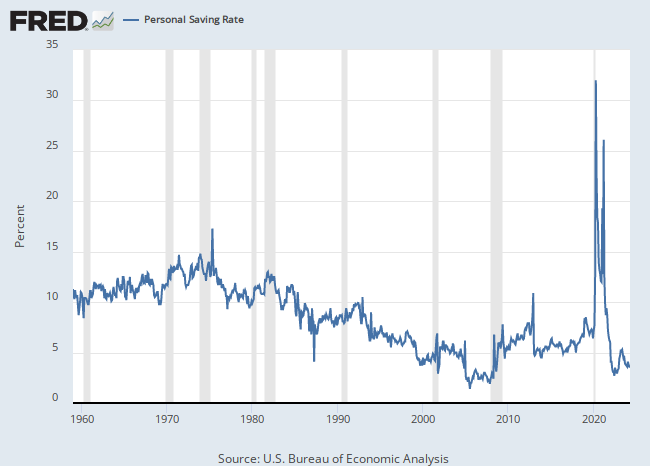

Now, it’s sometimes argued that because most workers no longer have access to defined benefit pensions, it’s unfair to call upon ordinary people to pay for pensions which go to middle class academics or public sector employees more generally. But this argument pits workers against each other when really they have a common interest in restoring the defined benefit pension model. In the US, defined benefit pensions have mostly been eliminated in the private sector in favour of the defined contribution 401ks and Roth IRAs. In most cases, these defined contribution plans are failing to leave workers with enough income to retire comfortably. The median 401k account contains less than $19,000. 74% of Americans worry about not having enough for retirement and 86% believe there’s a “retirement crisis”. A quarter of Americans over age 45 report having no retirement savings whatsoever and nearly half claim they would need to borrow money or sell something to pay for a $400 emergency. Even as retirement has become more dependent on private saving, US savings rates have plummeted, from more than 10% in the 1960s to just 2.5%:

As the retirement situation deteriorates, older people are compelled to remain in the labor force for much longer. Unable to retire, they stay on and take jobs which are needed by younger workers. Because the younger workers can’t get these jobs, they’re ending up underemployed and they’re struggling to enter the housing market. This depresses the economic potential and quality of life of an entire generation of people, reducing growth rates and making it harder still for this next generation to accumulate any significant amount of savings (much less the kind of savings which would allow them to retire). The switch from defined benefit pensions to defined contribution is gradually eliminating the possibility of retirement for many workers and creating a situation in which there are likely to be millions of elderly people with no retirement savings who are no longer physically capable of working. It’s a crisis which ravages the economic prospects of both young and old.

Defined benefit plans make it clear to society what the cost of retirement is going to be. If circumstances change we know how much funding we need to keep our promises to workers. But defined contribution plans conceal the extent to which workers aren’t prepared for retirement until it’s a crisis. At that point the state either has to bail out retirees all at once at great cost, or it has to cut them loose and leave them to struggle on National Insurance and Social Security alone, forcing many to remain in the workforce until their brains and bodies break down. That’s not good for them, nor is it any good for younger workers who will be crowded out of the best careers, forced onto lower earnings trajectories, and eventually deprived of their pensions in turn.

In defending the defined benefit pensions of academics, we help to defend defined benefit pensions more broadly for those who still retain them, and we draw attention to the need to solve the burgeoning retirement crisis faced by so many people in otherwise rich western democracies.

This is just one important reason to support the UCU strike. Part II and III will follow: