Last Week Tonight‘s John Oliver recently ran a segment in which he slated Jill Stein’s proposal to eliminate student debt through quantitative easing:

His criticism seemed to suggest that the Federal Reserve is obviously irrelevant in this policy area:

It’s basically akin to saying, ‘I’ll make us energy independent by ordering the Post Office to invade Canada.’ No, Jill. That’s impractical, it’s a terrible idea, and you don’t seem to understand anything about it.

Oliver, who is usually quite perceptive and well-informed, gets this wrong, and he gets it wrong in no small part because monetary policy is complicated and difficult to understand, both in terms of the economics and in terms of the politics. So let’s talk about how Stein’s idea works.

To understand why Stein thinks it might make sense to have the Federal Reserve eliminate student debt, you have to understand what quantitative easing is. Quantitative easing (or “QE” for short) is a form of unconventional monetary policy in which the central bank prints money and buys things with it to inject that money into the economy and encourage investment and consumption. Many people instinctively think that QE will generate inflation, but because QE is generally only introduced in economies that are already underperforming the large inflation does not materialize–QE is replacing investment and consumption that was lost during recessions rather than adding additional investment and consumption on top of what went before.

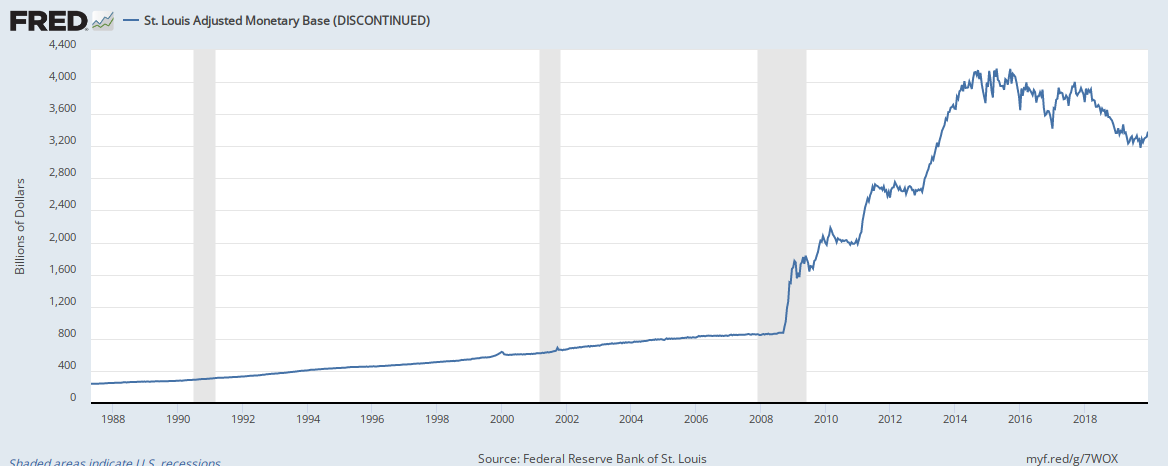

In the United States, QE was a big part of the response to the 2008 economic crisis. The Federal Reserve engaged in three rounds of QE. You can see them in the monetary base–it grew dramatically each time we did a round of QE:

Now, when we did these rounds of QE, the central bank decided to buy US treasuries from American banks. This means that for instance when the Obama administration borrowed money to fund the stimulus package in 2009, the banks that lent the government money would receive US treasuries, and then the Federal Reserve would buy back those treasuries in exchange for cash. This allows the government to spend money without crowding out private sector investment, and the banks love that. When the debt comes due, the government pays the debt holder, which is now the Federal Reserve instead of a bank. And of course any profit the Federal Reserve makes is by law delivered back to the treasury. This is a somewhat convoluted way by which the government funds partially funds stimulus spending through money printing. Indeed, in the 6 year period between 2008 and 2014, the Federal Reserve returned roughly $500 billion to the treasury, which is more than half of the cost of the stimulus package, and the Fed will continue to pay large sums to the treasury for some time:

The implications of this are very fun once you start to unpack it, as many economists working in Modern Monetary Theory (MMT) are now doing–these economists believe that the government could in theory cut out the middle man and fund all of its expenditures through money printing, using taxes only a means of controlling the inflation rate and influencing the distribution.

Stein is not proposing to fully embrace MMT. What she wants to do is get the Federal Reserve to buy student debt instead of (or in addition to) US treasuries. So the Fed would buy student debt from the banks (and from the federal government, which owns a lot of student debt) and then cancel it. This relieves the student debt burden and it prevents the banks from losing money in the process. The primary difference between this proposal and the QE we’ve done to this point is that if the Fed cancels the student debt, it can’t make money off of it which it can then send to the treasury. But if relieving student debt encourages young people to consume rather than pay down debt, it would encourage economic growth and that would have some positive effects on revenue.

The issues with the policy are more political–the Federal Reserve does not want to do this, and it currently enjoys a level of independence which prevents the President from dictating monetary policy to the Fed. However, the president could gradually replace the members of the Fed’s board of governors with people sympathetic to the policy or reform how the Fed works through legislation. There are two vacancies on the board of governors and 3 governors whose terms will expire before the 2024 election, so in theory a president could slowly pack the board with 4 governors (which would be a majority) by 2022 or 5 by 2024. The chair of the Fed is up for renewal or replacement in 2018. These paths are difficult but not in theory insurmountable. Given that a Stein presidency approaches political impossibility to begin with, it is bizarre to grant that assumption without further revising our assumptions about what would be politically feasible if Stein were somehow president. If Stein ran on this issue and somehow won, that would put a lot of political pressure on the Fed to accommodate it.

It’s a radical policy, but you could see how and why someone would want to do it. It’s not comparable to “telling the post office to make us energy independent by invading Canada”. The core inflation rate is still below the traditional 2% target and well below the more radical 4% target that’s been suggested in recent years by economists:

The employment-population ratio, which measures the share of the population that is in work, is mostly recovered but not all the way there:

The gap between productivity and wages is still significant:

You could make a case for some more stimulus, particularly stimulus which targets people at the bottom end of the economic distribution who have not been the primary beneficiaries of the growth we have seen since 2008–much of the monetary stimulus that has gone to the bankers through QE has arguably failed to trickle down.

This is not to say that Stein doesn’t have issues as a candidate–she sometimes indulges in lazy conspiracy theories about our regulatory agencies, wants to ban GMOs, and wants to cut defense by 83%. Unfortunately, the appropriate scrutiny these positions are receiving has encouraged people to dismiss the proposals she’s come up with that are legitimately interesting, and that will make it more difficult to build support for them in the future.